Australia consistently appears near the top of global property price rankings.

On some measures, we are one of the six most expensive countries to buy a typical apartment.

Our mean dwelling price hovered around $1 million in early 2025, while the average full‑time adult earned about $2,010 per week.

That gap between wages and property prices feels insurmountable for many households and prompts an obvious question: why are Australian homes so expensive?

In this opinion piece we unpack the structural drivers behind our high property prices and consider what they mean for home buyers, investors and renters.

We also touch on how you can take control of what you can change—your finance—and why it might be time to run your numbers through our Loan Optimiser.

The global context: high prices meet high incomes

International comparisons often frame Australia as a pricey housing market.

One recent global survey of 60 countries ranked us sixth for the price of a typical apartment per 100 m².

Our housing is cheaper than Switzerland and Norway but more expensive than many other wealthy nations.

At the same time, Australian incomes are among the highest in the world.

Full‑time workers earned roughly $2,010 per week in May 2025.

Even with dual incomes, though, stretching to a $1 million property can feel daunting.

That tension—between high incomes and even higher prices—forms the backdrop to our affordability debate.

High land values where people want to live

Australia is one of the world’s most urbanised nations, with most of us crammed along a narrow coastal strip on the east and south coasts.

Our population density is highest around Sydney, Melbourne and Brisbane, where harbourfronts, beaches and natural topography shape our lifestyles.

These natural features also impose strict limits on buildable land.

Combine limited coastal land with strict planning controls, heritage overlays and height restrictions, and the cost of a block in a blue‑chip suburb soars.

This is why Sydney’s eastern suburbs, the Lower North Shore and Melbourne’s Toorak command multi‑million‑dollar price tags.

People aren’t just paying for bricks and mortar; they are paying for access to amenity, views, prestigious school zones and proximity to jobs.

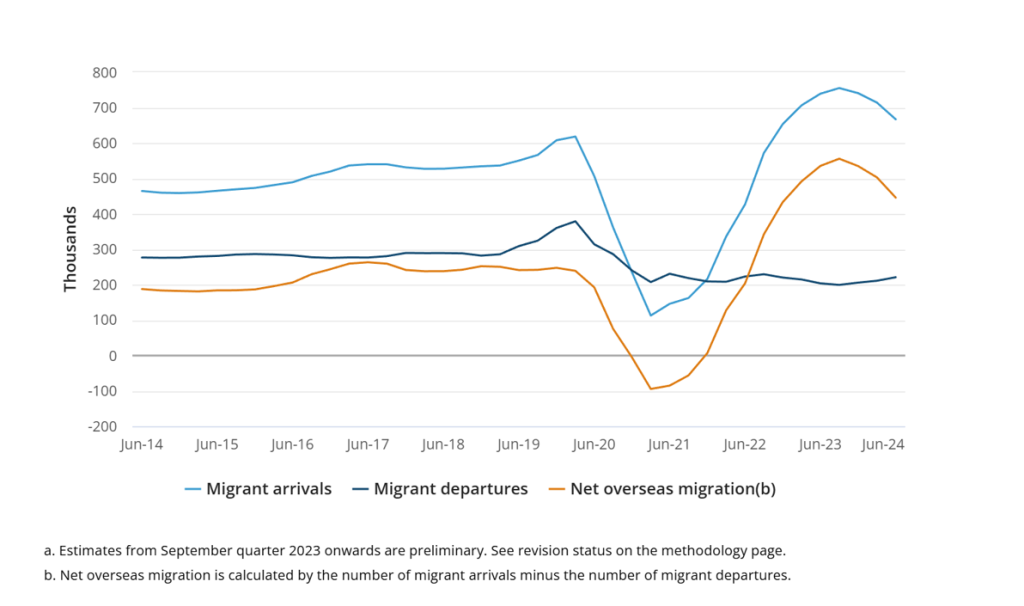

Population growth and migration

Demand doesn’t abate because the population keeps growing.

Australia attracts migrants from around the globe thanks to its economic stability, strong employment prospects and appealing lifestyle.

By mid‑2020s, net overseas migration was contributing hundreds of thousands of new residents each year.

International students and temporary workers add further strain to rental markets.

With supply slow to respond, increased demand inevitably pushes up prices and rents.

Construction bottlenecks and supply shortfalls

On paper, Australia often approves plenty of new housing, but the pipeline struggles to translate into completed dwellings.

The National Housing Finance and Investment Corporation (NHFIC) has warned of a shortfall of homes through 2025–27 because of capacity constraints—including labour shortages, material costs and slow planning approvals.

Even when land is zoned, it can take years to get shovels in the ground.

This means supply rarely keeps pace with population‑led demand.

The current construction industry environment, marked by high interest rates and collapses of major builders, further undermines new supply.

Ultimately, restricted supply in the face of strong demand drives prices higher.

Tax and financing settings

Australian tax policy also shapes property prices.

Domestic investors can deduct interest payments on investment loans against rental income (often referred to as negative gearing) and may receive a capital gains tax discount on profits when they sell.

These incentives encourage investment in residential property as a wealth‑building strategy.

Foreign investors, meanwhile, face stricter rules today than a decade ago—restrictions on buying established dwellings and higher application fees—but they can still buy off‑the‑plan apartments and new builds.

Australia’s reputation as a transparent real estate market with strong property rights makes it attractive to global capital despite higher entry prices.

Global investors love Australian real estate

Why would global investors pay top dollar for Australian property?

The reasons range from economic and policy stability to lifestyle and liveability.

Major cities such as Sydney, Melbourne, Adelaide and Perth consistently rank highly on global liveability indices, creating stable demand from expatriates and corporate relocations.

Robust population growth, low unemployment, and strong rental demand provide reliable yields, especially in apartment markets in Brisbane, Perth and regional centres.

Australia’s real estate market is also relatively transparent and liquid, reducing risk for overseas buyers.

Finally, investors know our market offers diversification: while Sydney’s yields can be slim, regional hubs and smaller capitals deliver cash flow, and long‑term capital growth remains positive across most cities.

The price map: most and least expensive

Housing affordability varies dramatically across the country.

In the September quarter of 2025, Sydney’s median dwelling value was roughly $1.26 million, keeping it the most expensive capital.

Melbourne’s median sat around $922,000, Canberra about $900,000, Brisbane $898,000, Adelaide $804,000 and Hobart $791,000.

Perth’s median hovered near $774,000, while Darwin remained the cheapest at around $519,000.

These figures shift month to month, but the ranking tends to be stable.

Within cities, prestige enclaves amplify the price gap.

In Sydney’s eastern suburbs (Point Piper, Vaucluse, Bellevue Hill), on the Lower North Shore or the Northern Beaches, a detached house routinely costs several million dollars.

Melbourne’s Toorak and Brisbane’s inner‑east riverfront also join the club of ultra‑expensive neighbourhoods.

At the top end, $1 million might buy only 45 m² of prime Sydney property, compared with 87 m² in Melbourne and over 100 m² in Perth or Brisbane.

Internationally, that same $1 million would secure a mere 19 m² in Monaco or 22 m² in Hong Kong.

These comparisons illustrate how tightly supply is constrained in prime Australian suburbs.

On the flip side, smaller capitals and regional centres offer more affordable entry points.

Darwin consistently posts the lowest capital city median values because its economy is smaller, job opportunities limited and climate more challenging.

The territory’s population is around 150,000 people in the urban area, meaning fewer buyers and less competition.

Rental yields there can look attractive, but capital growth has historically been weak and volatile.

If you’re hunting for a cheaper investment, you need to look for markets with stronger job growth, diversified economies and growing populations—qualities that Darwin often lacks.

Will property ever be affordable?

Nothing in housing is permanent, but some forces are stubborn.

The concentration of demand on the coast, restrictive planning regulations, construction constraints and continued migration are hard to unwind.

Unless supply increases significantly or demand moderates, Australia is likely to remain in the top tier of global property prices.

There are no obvious indicators that a price crash or sustained fall is imminent relative to wages growth.

As long as buyers value our lifestyle, stability and amenity, and as long as supply remains constrained, Australian real estate will attract strong local and foreign interest.

What this means for you

If you’re a first‑home buyer or investor, these structural realities can be both daunting and empowering.

On the one hand, waiting for prices to plummet is unlikely to be a winning strategy.

On the other hand, understanding the drivers of high prices can help you make more informed decisions.

Here are a few reflections:

- Focus on what you can control.

You can’t change global demand for Australian property or planning laws, but you can choose when and where to buy, how much to borrow and what interest rate you accept.

There are markets—regional towns, outer suburbs, smaller capitals—where affordability is still reasonable.

Do your research and be prepared to compromise on size, location or dwelling type. - Prioritise financial prudence.

With prices high, it’s tempting to stretch your borrowing capacity.

But high debt can make you vulnerable to rate hikes or income shocks.

Aim for a loan that keeps your repayments at a comfortable percentage of your income. - Use Loan Optimiser to stay ahead.

Given the high cost of property and the long time frames of mortgages, getting a good loan deal is crucial.

Property Dollar’s Loan Optimiser helps you compare interest rates, fees and repayment structures across lenders.

You can model different loan sizes, terms and rates to see how they impact your monthly repayments and total interest paid.

Regularly reviewing your loan can save you thousands over the life of your mortgage. - Consider diversification.

If you already own property in one of the expensive capitals, think about diversifying into another city or region with different growth and yield dynamics.

Perth and Brisbane have been reviving, while regional centres offer higher yields and lower entry costs.

Diversification can spread risk and improve cash flow. - Stay informed.

Markets shift and policies change.

Migration settings, tax incentives and planning reforms can alter the landscape.

Stay up to date through credible news sources and tools like Property Dollar’s market reports.

Being proactive can help you spot opportunities before the broader market reacts.

Final thoughts

Australian property is expensive because of a confluence of factors: scarce land in desirable locations, strong population growth, supply constraints, investor incentives and global demand.

These forces won’t disappear overnight, which means waiting for a crash is not a strategy you can bank on.

Instead, approach the market with a long‑term view, realistic expectations and a clear understanding of your own financial position.

To help you navigate high prices and rising interest rates, use the Loan Optimiser in the Property Dollar app.

It’s an easy way to check if your current loan is competitive, explore refinancing options and test different scenarios.

When every percentage point matters, making sure you have the right loan could be the difference between managing comfortably and feeling stretched.

Disclaimer: The views expressed in this article are opinion only and do not constitute financial advice.

You should consider your own circumstances and consult a qualified professional before making any financial decisions.