Important: This article is for informational purposes only and does not constitute financial advice. Always consult with a qualified financial advisor or mortgage broker before making investment decisions.

Quick question: What’s your loan-to-value ratio right now?

Not approximately. Not “around 70%, I think.” Your exact LVR across each investment property.

If you hesitated, you’re not alone. Most property investors would need to call their bank, request statements, research property values, and spend an hour calculating what should be an instant answer.

LVR isn’t some obscure technical metric. It’s as fundamental to property investment as revenue is to running a business or stock prices are to share investing. Yet most investors operate without knowing this critical number, and it’s costing them thousands in missed refinancing opportunities, higher interest rates, and suboptimal borrowing decisions.

The difference between amateur and professional investors isn’t intelligence or experience. It’s infrastructure. Professionals know their LVR continuously because they’ve automated the tracking. Amateurs check once or twice a year when forced to, then operate on stale data the rest of the time.

Let’s fix that.

What is LVR in Property Investment?

LVR stands for Loan-to-Value Ratio. It’s the percentage of your property’s value that you’ve borrowed from the bank.

The formula is simple:

LVR = (Current Loan Balance ÷ Current Property Value) × 100

Real example:

- Property value: $750,000

- Loan balance: $525,000

- LVR: ($525,000 ÷ $750,000) × 100 = 70%

This means you’ve borrowed 70% of the property’s value. The bank owns 70%; you own 30% (your equity).

Why it’s called loan-to-value: It measures your loan relative to the property’s current value. Higher LVR means more leverage (and more risk). Lower LVR means more equity (and less risk).

The critical insight most investors miss: LVR isn’t static. It changes constantly as property values fluctuate and as you pay down your loan. That $750,000 property might be worth $780,000 in six months. Your $525,000 loan might be $515,000 after six months of payments. Suddenly your LVR is 66%—but only if you’re tracking it.

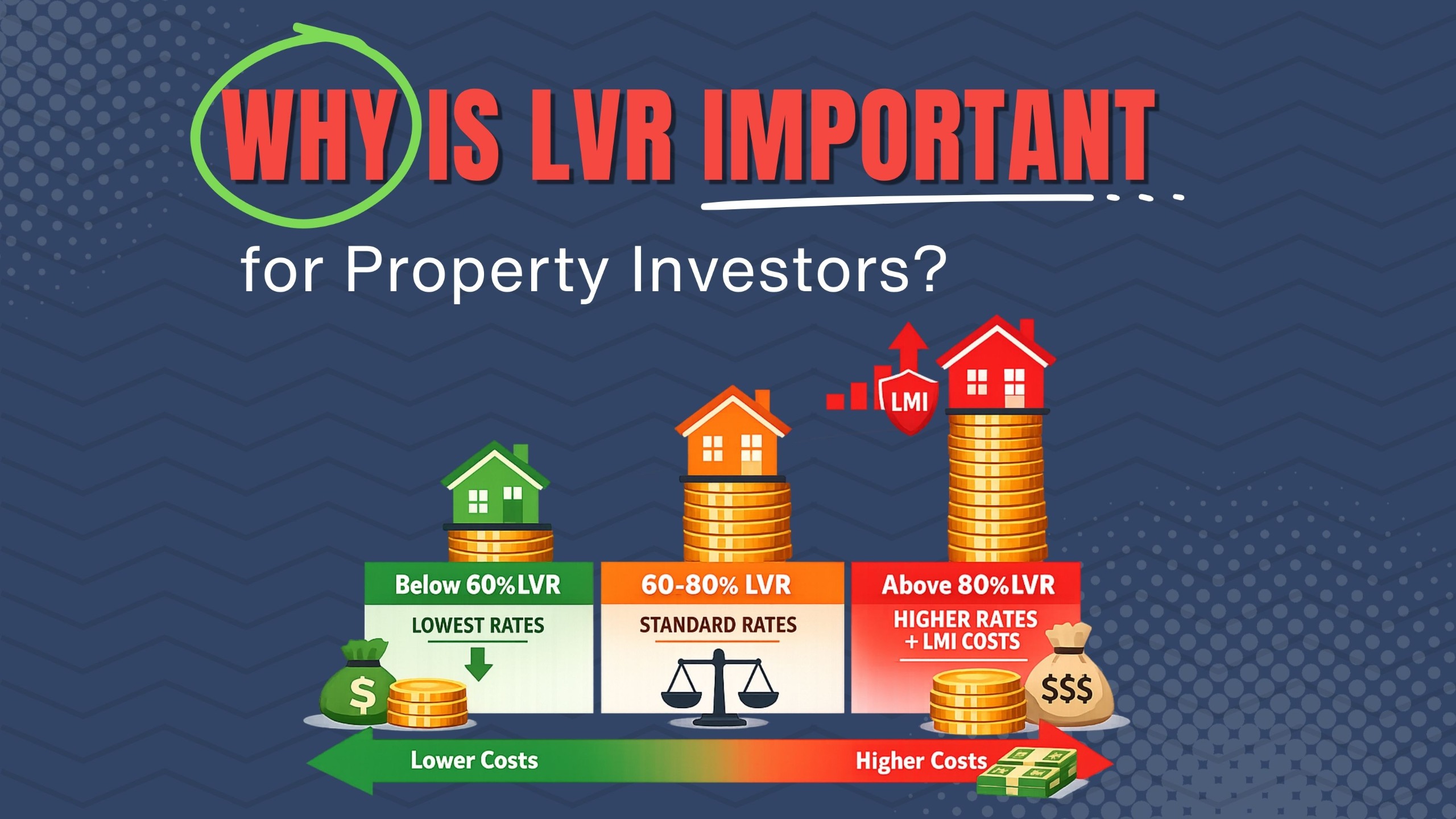

Why is LVR Important for Property Investors?

LVR isn’t just a number—it directly affects your wealth-building capacity and costs.

It Determines What You Can Borrow

Banks won’t lend beyond certain LVR limits. For investment properties, most lenders cap at 80% LVR (some go to 90-95% with expensive lenders mortgage insurance). Your current LVR determines whether you have borrowing capacity for your next purchase.

An investor at 65% LVR has significant room to borrow. An investor at 78% LVR has limited capacity. The difference between these positions might be the difference between buying your next property this year or waiting two more years.

It Affects Your Interest Rates

Banks price risk through LVR tiers:

- Below 60% LVR: Premium rates (lowest available)

- 60-80% LVR: Standard competitive rates

- Above 80% LVR: Higher rates plus LMI costs

Small LVR differences create large cost differences. Moving from 82% to 78% LVR on a $600,000 loan might save you $2,500-4,000 annually in interest and eliminate $18,000 in LMI costs.

It Triggers Lenders Mortgage Insurance

The most important threshold: 80% LVR.

Borrow 80% or less = no LMI required. Borrow more than 80% = LMI applies (typically $10,000-$30,000 depending on loan size).

Many investors pay LMI when purchasing at 85-90% LVR. After a few years of appreciation and principal payments, their LVR drops below 80%, but they don’t realise it because they’re not tracking. They miss the opportunity to refinance, eliminate LMI from their structure, and access better rates.

It Measures Your Risk Exposure

Portfolio-wide LVR shows your total leverage position. An investor with three properties at 75% LVR is more vulnerable to market downturns than one at 60% LVR. Professional investors monitor this religiously to ensure they’re not overextended.

How Do You Calculate Your LVR?

The math is straightforward, but getting the inputs isn’t.

Step 1: Get your current loan balance

- NOT what you originally borrowed

- Your balance TODAY after all payments

- Requires logging into your lender’s portal (or calling them)

Step 2: Get your current property value

- NOT what you paid for it

- Current market value today

- Requires research: Domain/REA estimates, recent sales, or agent appraisals

Step 3: Calculate

Example:

Current loan: $547,000

Current value: $785,000

LVR: ($547,000 ÷ $785,000) × 100 = 69.7%

Common mistakes investors make:

Using purchase price instead of current value: “I paid $680,000, I owe $510,000, so 75% LVR.” Wrong if the property is now worth $750,000 (actual LVR: 68%).

Using original loan instead of current balance: “I borrowed $550,000 on a $700,000 property, so 78.6% LVR.” Wrong if you’ve paid it down to $515,000.

The calculation is easy. Getting accurate, current numbers is hard—which is why most investors don’t know their LVR.

What is a Good LVR for Investment Property?

There’s no universal “good” LVR—it depends on your strategy, age, and risk tolerance.

Below 60% LVR: Conservative

- Lowest rates available

- Maximum borrowing flexibility

- Strong buffer against market downturns

- Best for: Risk-averse investors, those nearing retirement

60-70% LVR: Balanced

- Competitive rates

- Reasonable leverage for growth

- Decent equity buffer

- Best for: Most investors in the wealth-accumulation phase

70-80% LVR: Growth-Focused

- Strong leverage for wealth building

- Still avoid LMI costs

- Less buffer, higher risk

- Best for: Younger investors, high-income earners

Above 80% LVR: Aggressive

- Triggers LMI (expensive)

- Higher interest rates

- Significant risk exposure

- Best for: First-time investors with limited capital (but risky)

Professional investors track both individual property LVRs and portfolio-wide LVR. You might have two properties at 65% LVR and one at 82%, giving a portfolio average of 70.7%. Both individual and total metrics matter.

Why Don’t Most Investors Know Their Current LVR?

The obstacles are real:

Getting loan balances is friction-heavy:

- Different portal for each lender

- Password resets, two-factor authentication

- Balance information buried in account details

- Multiple properties = multiple logins, multiple headaches

Getting property values requires estimation:

- Domain/REA estimates (often inaccurate by $50k+)

- Agent appraisals (cost money, take time)

- Recent comparable sales (requires research)

- Never 100% certain until the actual sale

The calculation takes effort:

- Even with both numbers, you need to calculate manually

- Spreadsheets that break

- Easy to make errors

- By the time you finish, the data is already outdated

The multi-property multiplier:

- One property: Tedious but manageable

- Three properties: Three times the effort

- Five properties: So overwhelming, people avoid it entirely

Most investors fall into the “I’ll do it later” trap. Months pass. They only check when forced to (refinancing application, tax time, new purchase). The rest of the year, they operate blind.

The Cost of Not Knowing Your LVR

Missed refinancing opportunities: You cross from 81% to 77% LVR in March, but don’t discover it until November. You could have refinanced in March and saved $2,800 on better rates. You lost eight months of savings ($1,867) because you weren’t tracking.

Delayed investment decisions: An opportunity arises, but you don’t know if you have borrowing capacity. By the time you gather data and calculate LVR (one week later), the property is under contract to a faster investor.

Paying unnecessary LMI: You’re still at 82% LVR (or so you think), so you accept LMI on your next purchase. Actually, you’re at 78% LVR—you could have avoided $16,000 in LMI entirely.

Suboptimal leverage strategy: You have three properties, but don’t know which has the best LVR for drawing equity. You leverage the wrong property, paying higher rates when you could have used the one at 64% LVR instead of 76%.

These aren’t theoretical scenarios. They happen constantly to investors who don’t track LVR systematically.

How Often Should You Check Your LVR?

The professional standard: Continuously, through automated tracking.

The practical minimum: Monthly, if you’re checking manually.

What most investors do: Once or twice annually, when forced to.

Why quarterly isn’t enough: Too much changes in three months. Property values shift. Loan balances decrease (on P&I loans). You miss optimal refinancing windows.

Why annual is completely inadequate: Twelve months of missed opportunities. Massive changes in property values possible. Operating blind 11 months out of 12.

The technology exists for continuous visibility. There’s no reason to accept anything less.

Can You Automate LVR Tracking?

Yes—and professional investors already do.

What automation requires:

- Current loan balances via Open Banking

- Current property valuations via automated models

- Automatic calculation (simple math, done automatically)

- Dashboard display (always visible, always current)

How Open Banking enables this:

- Securely connects to your lenders

- Retrieves current loan balances automatically

- Updates regularly without manual effort

- No more password juggling across multiple banks

How automated valuations work:

- Recent comparable sales data

- Market trends and suburb analytics

- Algorithm-based estimation

- Updated regularly with market movements

- Accurate enough for LVR tracking purposes

The experience difference:

Manual method:

- Log into Bank A (find password, 2FA authentication)

- Find loan balance: $547,230

- Log into Bank B (repeat password process)

- Find loan balance: $389,670

- Research Property 1 value: ~$785,000

- Research Property 2 value: ~$620,000

- Calculate LVR Property 1: 69.7%

- Calculate LVR Property 2: 62.9%

- Total time: 45-60 minutes

Automated method:

- Open app

- See all LVRs updated automatically

- Total time: 5 seconds

The choice is obvious.

How Property Dollar Helps Track Your LVR

For investors managing multiple properties, knowing your LVR position continuously isn’t optional—it’s fundamental infrastructure.

Property Dollar provides automated LVR tracking through Open Banking integration that connects to your home loan accounts and retrieves current balances automatically. Combined with property valuation data, this enables real-time LVR calculations across your entire portfolio.

Instead of spending an hour gathering data from multiple sources, you open the app and see your current position instantly. Every property. Every loan. Portfolio-wide LVR. Always current.

This isn’t about impressive technology—it’s about having reliable data when you need it. Professional investors don’t operate on guesswork or approximations. They have systems that deliver current information automatically.

At $9.99/month, Property Dollar Premium provides the infrastructure serious investors need: automatic loan tracking, real-time LVR visibility, and the data foundation that informs good decisions. It’s the difference between checking your LVR twice a year and knowing it continuously.

From “I Think” to “I Know”

So, back to the opening question: What’s your LVR right now?

If your answer is still “around 70%, I think”—you’re operating like most investors. But “most investors” aren’t building substantial wealth efficiently. They’re missing refinancing opportunities, paying unnecessary costs, and making decisions based on stale data.

Professional investors know their LVR precisely, continuously, and effortlessly. Not because they’re obsessive, but because they understand that fundamental decisions require fundamental data.

The three LVR truths:

- LVR isn’t optional information—it’s foundational. Like a business owner knowing revenue or a stock investor knowing portfolio value.

- Not knowing your LVR costs you real money. Missed refinancing opportunities, higher rates, delayed investments, suboptimal leverage—these add up to thousands annually.

- Technology has eliminated all excuses. Open Banking, automated valuations, and portfolio platforms make continuous LVR tracking effortless.

The question isn’t whether you should know your LVR. It’s why you’re still operating without knowing.

Time to stop calling your bank for answers you should have at your fingertips.

Final reminder: This information is general in nature and should not be considered personalised financial advice. LVR thresholds, lending policies, and refinancing opportunities vary by lender and individual circumstances. Always consult with qualified mortgage brokers and financial advisors before making decisions about borrowing, refinancing, or property investment strategies.